First Watch Restaurant Group (FWRG)·Q4 2025 Earnings Summary

First Watch Beats Q4 Revenue; CFO Retiring, New Menu Rollout Underway

February 24, 2026 · by Fintool AI Agent

First Watch Restaurant Group (NASDAQ: FWRG) reported Q4 2025 results that beat revenue estimates by 2.2%, driven by aggressive unit expansion and positive same-store sales. Two major announcements dominated the call: CFO Mel Hope is retiring after eight years, and the company just launched its first major core menu redesign in nearly a decade. Despite the beat, conservative 2026 guidance and traffic headwinds weighed on shares.

Did First Watch Beat Earnings?

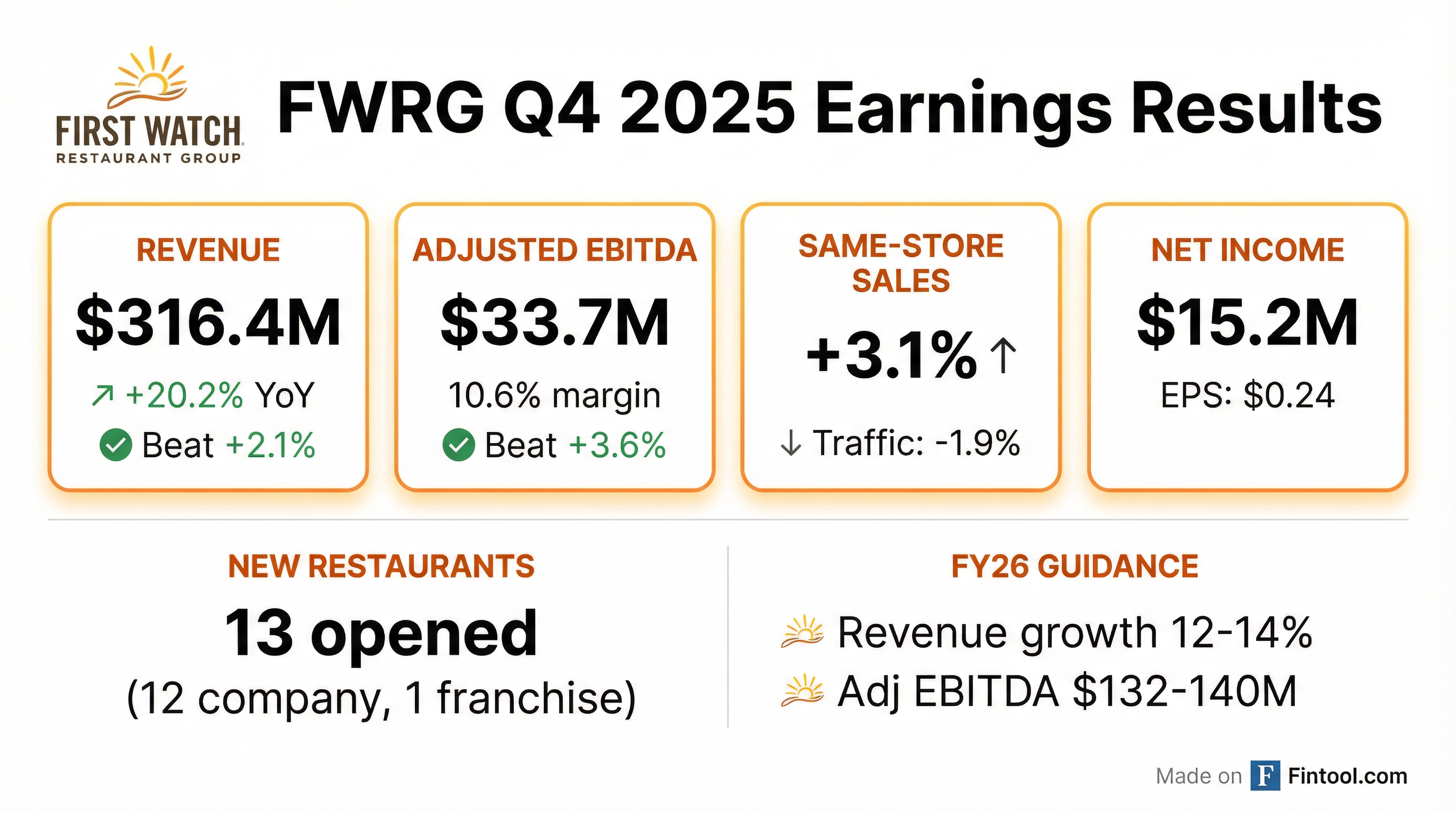

Revenue beat, EPS distorted by tax benefit. First Watch delivered Q4 revenue of $316.4 million versus consensus of $309.6 million, a 2.2% beat.

Net income context: The surge in net income was driven by a $10.7 million income tax benefit in Q4 2025 versus a $39K expense in Q4 2024. Excluding this one-time item, underlying profitability improvement was more modest.

Restaurant-level operating profit margin expanded 20 bps to 19.0%, demonstrating solid four-wall economics despite inflationary pressures.

What Did Management Say?

CEO Chris Tomasso highlighted the company's execution across multiple fronts:

"2025 was a year of significant progress on a number of fronts for First Watch. In addition to continuing our industry-leading new restaurant growth of nearly 11%, we increased total revenues by more than 20%, which included same-restaurant sales growth of 3.6% and positive same-restaurant traffic. As we look to 2026 and beyond, we are energized by the growth opportunities across all facets of our business, particularly the expansion of our evolving digital marketing platform."

Key callouts:

- Industry-leading unit growth of ~11%

- Digital marketing platform expansion as a 2026 priority

- Long-term target of 2,200+ restaurants nationwide

What's New This Quarter?

CFO Mel Hope Retiring

Material management change. CFO Mel Hope announced his retirement after eight years with First Watch, including leading the company through its 2021 IPO.

- Executive search begins immediately

- Hope will remain as CFO until successor is hired and onboarded

- Will serve as advisor through year-end 2026 to ensure seamless transition

CEO Tomasso: "Mel's been with First Watch since 2018 and was a critical part of our IPO in 2021. While he will certainly be missed, I'm optimistic about our company's promising future."

New Core Menu Launch

First major redesign in 10 years. In early February 2026, First Watch rolled out a redesigned core menu to all restaurants — the most significant menu overhaul since ~2016.

Permanent additions from seasonal menu:

- Barbacoa Breakfast Tacos and Barbacoa Chilaquiles Breakfast Bowl (premium protein)

- Strawberry Tres Leches French Toast (best-performing sweet item)

- Holey Donuts (new shareable)

- Customer-requested add-ons and improved navigation

Back-of-house benefits:

- Removed slow-moving items and single-use SKUs

- Reduced complexity and prep time

- Leverages "muscle memory" from previous seasonal execution

CEO Tomasso noted the last major menu overhaul ~10 years ago coincided with the acceleration of growth, and early test results show positive mix upside from the new menu — one reason management elected not to take pricing in Q1.

Marketing Platform Expansion

The digital marketing pilot tested in ~1/3 of comparable restaurants in 2025 delivered compelling results: several hundred basis points traffic lift in test vs. control markets, with increases in both aided and unaided awareness.

2026 rollout:

- Expanding to "vast majority" of comp base

- Strategy: Target breakfast daypart users who aren't yet First Watch customers

- Channels: Connected TV, online video, paid search, programmatic digital

- Focus on driving trial, then nurturing to first-party connection and in-restaurant visits

What Did Management Guide?

First Watch provided FY 2026 guidance that came in at the lower end of long-term targets:

Guidance vs. consensus: The FY 2026 Adjusted EBITDA guidance of $132-140 million brackets the current Street estimate of ~$140 million, suggesting limited upside to expectations.

Conservative comp guidance: The 1-3% same-store sales outlook is notably below the long-term target of ~3.5%, reflecting management's caution on traffic trends. Black Box Intelligence projects ~3% industry-wide same-restaurant traffic decline in 2026, yet First Watch expects to outperform the industry as it has historically.

What Changed From Last Quarter?

Traffic inflection not sustained. After posting positive same-store traffic of +2.6% in Q3 2025, First Watch saw traffic turn negative again at -1.9% in Q4. This reversal suggests the traffic recovery was partially seasonal rather than structural.

Margin trajectory: Restaurant-level operating profit margin of 19.0% in Q4 2025 improved from 18.8% in Q4 2024, but remains below the 20.1% achieved in FY 2024. Full-year margin compressed to 18.5% from 20.1% as the company invested in growth.

How Did the Stock React?

First Watch shares are trading lower following the earnings release:

Why the sell-off? Despite the revenue beat, the market appears disappointed by:

- Negative Q4 traffic (-1.9%) after positive Q3 traffic

- Conservative 1-3% same-store sales guidance for FY 2026

- Slower EBITDA growth implied by guidance (~9-16% vs. mid-teens long-term target)

Unit Growth Remains the Story

First Watch's differentiated daytime-only model continues to fuel rapid expansion:

2025 class is outperforming. The 64 restaurants opened in 2025 are running 19% above underwriting targets on first-year sales — the strongest performance in company history. The Cosner's Corner, Virginia location set a record with $90,000+ in first-week sales.

New unit economics remain attractive:

- Year 3 Average Sales: $2.8M

- Year 3 Restaurant-Level Operating Profit: 18-20%

- Year 3 Cash-on-Cash Returns: ~35%

- IRR: 18%+

Five new markets entered in 2025: New England, Las Vegas, Salt Lake City, Boise, and Memphis — together representing up to 155 additional unit opportunities. The Boston flagship opened on Boylston Street in January 2026 to establish brand visibility.

2026 strategy: Shift from market entry to market densification — deepening presence in newly entered markets while filling in core and emerging markets. Development pipeline is "essentially scheduled" for 2026, with site selection already underway for 2027 and 2028.

Full-Year 2025 Performance

Q&A Highlights

On 2026 pricing strategy: Management elected not to take price in January 2026, a departure from prior years. Carried pricing is ~4% in H1, blending to ~2% for full year. The decision was driven by (1) favorable commodity outlook and (2) expected mix upside from the new core menu. Mid-year pricing remains a lever if needed.

On commodity inflation: Full-year 2026 commodity inflation guided at 1-3%, driven by coffee and bacon, partially offset by expected deflation in eggs and avocados. Inflation expected to be somewhat higher in H2 than H1.

On year-to-date trends: CEO Tomasso noted "year-to-date trends are improved versus December" and the company believes it's on track to meet annual same-store sales guidance.

On daypart performance: Weekday breakfast showed strength throughout 2025 after weakness in 2024. Weekends also slightly outperformed in Q4 and full year.

On delivery channel: Third-party delivery was a 2025 success, achieving both transaction growth and margin goals — without funding free delivery. Management believes the delivery occasion is "largely incremental" and helps keep the brand top-of-mind for eventual in-restaurant visits.

On tax refund sensitivity: Management believes their customer demographic (higher household income) isn't highly sensitive to tax refunds, unlike quick-service restaurants.

On G&A leverage: Cash-based G&A expected to lever as growth continues, but new equity compensation program (expanded to divisional operators) may limit total G&A leverage in 2026. The equity program doesn't impact Adjusted EBITDA.

On restaurant-level margins: Getting back to the high end of the 18-20% range would require accelerating margin maturation at newer restaurants. Management won't sacrifice customer experience for speed, but sees opportunity over time. Current consolidated margin is impacted by high-volume new restaurants still on the maturity curve.

Key Risks and Concerns

Traffic remains the achilles heel. While FY 2025 achieved +0.5% traffic growth, this was heavily weighted to Q2/Q3. Q4's -1.9% traffic decline and conservative 2026 guidance suggest management expects traffic pressures to persist.

Margin pressure from growth investments. Adjusted EBITDA margin compressed 130 bps YoY to 9.9% as the company invested in growth infrastructure, pre-opening costs, and G&A to support expansion.

Franchise contraction. Franchise-owned restaurants declined from 83 to 73, with the company continuing to acquire franchise locations. This reduces franchising income but improves control and unit economics.

CFO transition risk. With Mel Hope retiring after leading the company through its IPO, the search for a new CFO introduces execution risk during a period of aggressive growth. The extended transition timeline (advisor through year-end 2026) mitigates but doesn't eliminate this risk.

Forward Catalysts

- New core menu rollout — First major redesign in 10 years, launched Feb 2026, showing positive mix in tests

- Digital marketing platform expansion — Scaling from 1/3 to majority of comp base; delivered hundreds of bps traffic lift in tests

- New unit openings — 59-63 planned for FY 2026, maintaining ~10% unit growth

- Long-term runway — 2,200+ restaurant opportunity vs. 633 today (~3.5x expansion potential)

- Seasonal menu innovation — Current features include Chimichurri Steak & Eggs Hash and the returning B.E.C. sandwich

Culture and talent: Named America's #1 Most Loved Workplace (2024, 2025) and Glassdoor's Top 25 Best Places to Work in Consumer Services (2026). Employee turnover declined in 2025 with 40% increase in applicant volume.

First Watch operates exclusively during daytime hours (7 a.m. to 2:30 p.m.), serving breakfast, brunch, and lunch. The company has grown from a single restaurant in 1983 to 633 locations across 32 states.

Related Links: